Risk management is critical in modern banking, especially as they navigate volatile markets, rising regulatory expectations, and increasingly sophisticated fraud threats. Banks today operate in an interconnected environment where even a single unmanaged risk, whether a borrower default, market disruption, a cyberattack, or a compliance failure, can escalate into significant financial losses and broader economic impact.

Strengthening governance, adopting advanced technologies, and improving operational resilience enables banks to safeguard operations while supporting the stability of the financial ecosystem.

This article explores the key risks faced by banks, the techniques used to analyze them, and the best practices that support effective risk management.

Banking Risk Management Framework

A banking risk management framework provides a structured approach to identifying, assessing, monitoring, and mitigating risks that threaten institutional performance and compliance. It also establishes governance standards and oversight mechanisms aligned with global regulatory expectations.

This framework enables institutions to manage exposures across credit, market, operational, liquidity, and compliance areas with greater precision. It also reinforces governance through risk committees and Chief Risk Officers (CROs), ensuring consistent oversight and regulatory alignment. When effectively implemented, it supports informed decision-making, efficient capital allocation, and sustained stakeholder confidence.

Regulatory Foundations of Risk Management

Banking risk practices draw from globally accepted standards that define expectations for capital, liquidity, and governance. Frameworks issued by the Basel Committee on Banking Supervision, along with supervision from central banks and institutions such as the Bank for International Settlements, set clear benchmarks for financial strength and risk oversight.

AML and KYC requirements translate these expectations into operational controls through customer verification, transaction review, and reporting obligations. These standards bring consistency to risk practices, improve accountability, and support stability across the banking system.

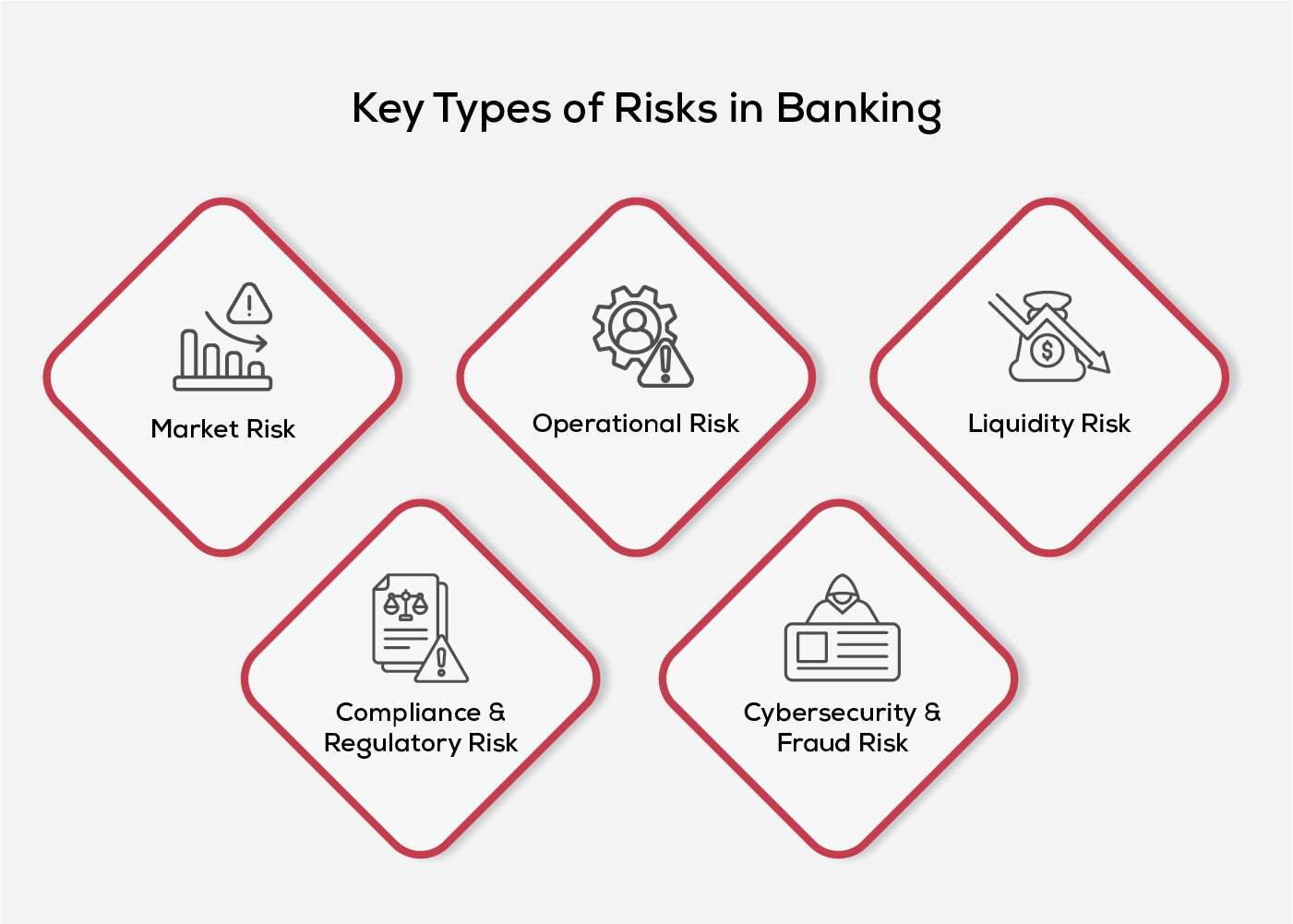

Key Types of Risks in Banking

Risk categories in banking are grouped based on their source and impact, enabling clearer and consistent analysis. This classification supports structured evaluation, comparability across business units, and more disciplined reporting.

Market Risk

Adverse movements in interest rates, foreign exchange rates, or equity prices can erode earnings and reduce asset valuations. Such volatility can compress margins and weaken portfolio performance, particularly in uncertain economic conditions. Prolonged exposure to unfavorable market shifts can also affect capital adequacy and overall financial positioning.

Operational Risk

Failures in internal processes, systems, or human execution can disrupt critical operations and expose the bank to financial and reputational damage. Incidents such as system outages, processing errors, or internal fraud can lead to service interruptions and regulatory scrutiny. Repeated breakdowns may also weaken stakeholder confidence and increase compliance pressure.

Liquidity Risk

Inadequate access to cash or liquid assets can prevent a bank from meeting short-term obligations as they fall due. This risk becomes more pronounced during periods of sudden withdrawals or restricted funding access. Sustained liquidity stress can force asset fire sales, impact funding costs, and strain overall financial stability.

Compliance & Regulatory Risk

Non-compliance with legal and regulatory requirements can result in financial penalties, operational constraints, and reputational harm. Gaps in adherence to standards such as Anti Money Laundering (AML), Know Your Customer (KYC), or capital adequacy norms may trigger heightened supervisory action. Persistent lapses can also limit business expansion and weaken market credibility.

Cybersecurity & Fraud Risk

Cyberattacks and fraudulent activities can compromise sensitive data, disrupt banking services, and lead to direct financial losses. Threats such as phishing, account takeovers, and data breaches have become more frequent with the expansion of digital banking. These incidents can significantly undermine customer trust and brand reputation.

Risk Assessment & Measurement Techniques

Evaluating risk requires a clear understanding of how exposures may affect the bank under different conditions. Banks use structured methods and analytical tools to interpret potential impact, compare risk levels, and identify areas that require closer attention. This enables more informed decisions and improves overall visibility across risk functions.

Qualitative vs. Quantitative Risk Assessments

Banks integrate both approaches, with qualitative insights informing model assumptions and quantitative outputs supporting risk limits, reporting, and regulatory compliance.

They rely on qualitative assessments to capture risks that are difficult to model, such as governance gaps, conduct issues, or emerging threats where historical data is limited. These evaluations are typically embedded in internal control reviews, audit findings, and risk and control self-assessments (RCSAs), where expert judgment plays a central role.

Quantitative approaches are applied where exposures can be measured using reliable data, particularly in areas such as market and credit risk. Techniques such as scenario analysis and Value-at-Risk (VaR) are used to estimate loss ranges, assess sensitivity to market movements, and support capital planning.

Risk Modelling & Stress Testing

Risk models enable banks to evaluate how changes in market conditions or economic downturns can affect their financial position. Stress testing plays a key part of this process that allows banks to simulate extreme but possible scenarios to see how their portfolios and capital levels would withstand pressure. These techniques help banks prepare for stress events and ensure stability during periods of economic strain.

Risk Scoring & Monitoring Systems

Banks use internal scoring models to assess the risk associated with customers, transactions, and operational activities. These scores are tracked through automated monitoring systems that detect unusual patterns and trigger alerts for review when set thresholds are exceeded. Tools such as fraud detection platforms, credit risk models, and liquidity indicators including the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) support timely intervention and more informed decision-making.

Internal Controls & Audits

Internal controls establish structured processes to limit errors, prevent fraud, and support reliable day-to-day operations. Internal audits periodically review these controls to assess their effectiveness and ensure adherence to regulatory requirements. They also highlight gaps and areas requiring corrective action. Together, controls and audits strengthen operational discipline and reduce exposure to financial and compliance risks.

Best Practices for Risk Mitigation in Banking

Effective risk mitigation depends on how consistently risk disciplines are applied across governance, operations, and business functions. Institutions that maintain clear standards and accountability are better positioned to manage exposures and respond to change.

1. Enterprise-Wide Risk Framework

Establish a unified framework to bring consistency to risk practices across business units. Define roles, reporting lines, and standardized methods to reduce fragmentation and improve coordination. Support timely response to emerging issues and maintain alignment with business priorities.

2. Risk Monitoring into Core Operations

Integrate monitoring into operational workflows to identify risks as activities occur. Track key indicators continuously to surface deviations early and enable timely action. Strengthen day-to-day control without introducing parallel processes.

3. Continuous Compliance Alignment

Maintain up-to-date policies and controls in line with changing regulatory requirements. Conduct periodic reviews and apply centralized supervision to ensure consistency across functions. Reduce exposure to penalties and support adherence to applicable standards.

4. Digital and Cyber Resilience

Strengthen technology environments through continuous system surveillance, controlled access, and routine testing. Limit vulnerabilities and support uninterrupted service delivery across digital channels.

5. Risk with Business Decisions

Align risk considerations with core business activities such as lending, investments, and product development. Incorporate risk perspectives at the point of action to support balanced outcomes and avoid misaligned exposures.

Conclusion

The future of risk management in banking will depend on how effectively institutions adapt to a more dynamic and interconnected financial environment. As risk conditions become less predictable and regulatory expectations continue to rise, banks will need more agile frameworks, stronger visibility across operations, and faster response capabilities. The focus is steadily shifting from reactive risk handling to continuous risk intelligence supported by technology and coordinated governance.

Platforms such as Komply360 support this transition by streamlining compliance processes, improving oversight, and centralizing risk intelligence across the institution. Capabilities spanning AML/KYC workflows, risk monitoring, and regulatory reporting help banks strengthen operational control while reducing manual inefficiencies.

Banks that combine structured risk practices with integrated technology platforms will be better positioned to respond to changing market conditions, strengthen institutional resilience, and maintain long-term operational stability

Frequently Asked Questions

1. What’s the difference between ERM and traditional, siloed risk management?

ERM takes a bank?wide view of risk, using one framework and shared rules across all departments. Siloed risk management treats each area separately, which canseparately, which can miss how risks connect. ERM helps leadership see the full picture and make better trade?offs.

2. How often should a bank run stress tests?

A good practice is to run enterprise stress tests at least annually, with targeted or ad?hoc tests during market volatility, product launches, or major policy changes. Frequent lightweight scenario quarterly or even monthly checks help catch early warning signs.

3. What is a risk culture, and how do banks build it?

Risk culture is how people in the bank think about and act on risk every day. Banks build it by setting a clear risk appetite, training teams, rewarding good risk behavior and making it easy to speak up about issues without fear.

4. How do banks manage third?party or vendor risk?

They assess vendors before onboarding, add risk clauses in contracts, and monitor performance and incidents over time. Critical vendors may need independent audits, cyber assessments and clear exit plans if risk rises.

5. What are KRIs and how are they used?

Key Risk Indicators (KRIs) are simple metrics that signal rising risk like fraud alert rates, system downtime, or early?delinquency trends. Banks set thresholds and review KRIs regularly so teams can act before issues turn into losses.