Core banking technology has become a cornerstone of modern banking, enabling financial institutions to support evolving customer expectations, regulatory requirements, and digital transformation initiatives.

As banks continue to modernize their technology landscape, choosing the right core banking system has become a strategic decision that requires careful evaluation of functionality, integration capabilities, security, scalability, deployment models, and vendor support.

This guide explains what core banking system is and explores the key factors to consider when selecting a CBS that aligns with your institution's operational needs and long-term technology strategy.

What is a Core Banking System

Core Banking Systems operate as centralized back-end platforms that enable a wide range of financial functions, including processing transactions such as loans, deposits, and interest calculations across multiple branches. By connecting geographically distributed branches through a unified system, core banking technology ensures seamless operations and consistent service delivery.

In the era of digital banking, these systems play a crucial role in empowering customers. They enable individuals to access their accounts, perform transactions, and manage finances anytime and from anywhere, offering greater convenience and control.

As banks expand digital channels and introduce new financial services, the capabilities of their core banking system increasingly influence operational agility, regulatory compliance, and customer experience.

Why is Core Banking System Important

Core banking systems are essential for improving operational efficiency and scalability in financial institutions. By automating processes that were once manual, they reduce dependency on human intervention and significantly speed up transaction processing times. This efficiency allows banks to expand their services to remote and underserved regions without compromising quality.

A well-implemented core banking system minimizes the risk of interruptions and protects against potential security breaches. For financial institutions, choosing the right system is critical, as it directly impacts maintenance costs, regulatory compliance, customer trust, and revenue generation.

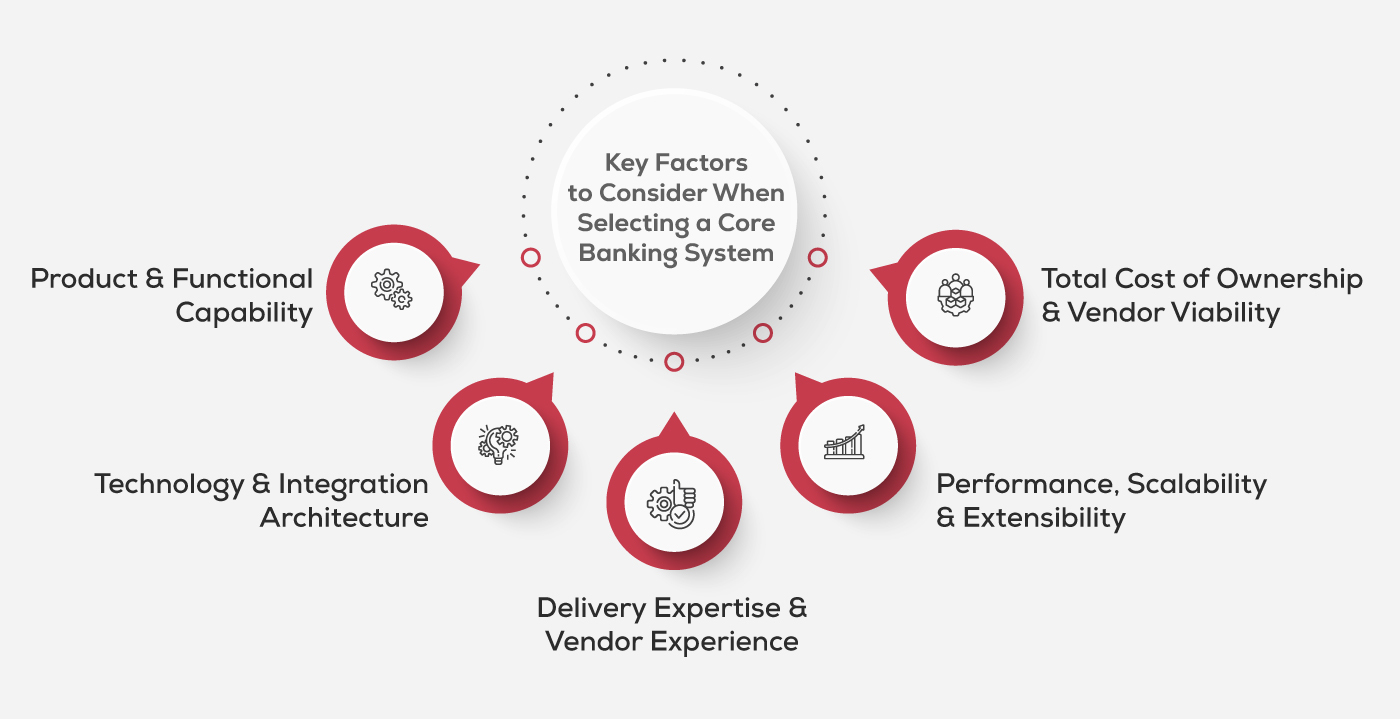

Key Factors to Consider When Selecting a Core Banking System

Selecting a core banking system extends beyond comparing software features. Financial institutions need to evaluate how well a solution aligns with their business strategy, regulatory obligations, integration requirements, and long-term technology roadmap. Since a core banking platform supports multiple business functions and remains in service for many years, the selection process requires a balanced assessment of both business and technical considerations.

The following factors can help banks identify a core banking platform that meets current operational needs while supporting future growth and transformation initiatives.

1. Product & Functional Capability

Evaluate whether the platform offers the flexibility to configure and deliver banking products that align with the institution's business model. Consider if it supports the bank's target customer segments such as retail, MSME, SME, mid-market, and corporate banking, while providing advanced capabilities where required, including functions like syndicated lending. It is equally important to review the vendor's product roadmap to ensure it aligns with the bank's long-term business objectives and evolving market requirements.

2. Technology & Integration Architecture

Assess the platform's technology architecture to determine whether it supports cloud-native deployment, scalability, resilience, and operational flexibility. Look for open integration capabilities, including APIs and webhooks, that enable seamless connectivity with payment networks, third-party applications, and the broader open banking ecosystem. The vendor's investment in emerging technologies such as Artificial Intelligence, automation, and real-time analytics is another important consideration, as it reflects the platform's ability to support future innovation.

3. Delivery Expertise & Vendor Experience

Consider the implementation partner's experience in delivering core banking transformation programs of similar scale and complexity. Review its track record, availability of certified resources, and understanding of the local regulatory and operational environment. It is also worth assessing the partner's governance framework, implementation methodology, and risk management practices, as these play a significant role in ensuring successful project execution.

4. Performance, Scalability & Extensibility

Verify that the platform can consistently handle high transaction volumes without compromising performance, availability, or operational resilience. Evaluate its ability to support future expansion through flexible deployment options, seamless integration with complementary banking solutions, and an extensible architecture that accommodates evolving business and technology requirements. A well-established partner ecosystem can further simplify the adoption of additional capabilities as business needs evolve.

5. Total Cost of Ownership & Vendor Viability

Assess the vendor's long-term viability by reviewing its financial stability, product vision, and continued investment in innovation. In addition to upfront implementation costs, evaluate the total cost of ownership, including licensing, maintenance, support, upgrades, and ongoing operational expenses. Flexible commercial models and sustainable maintenance approaches can provide greater long-term value while supporting the platform throughout its lifecycle.

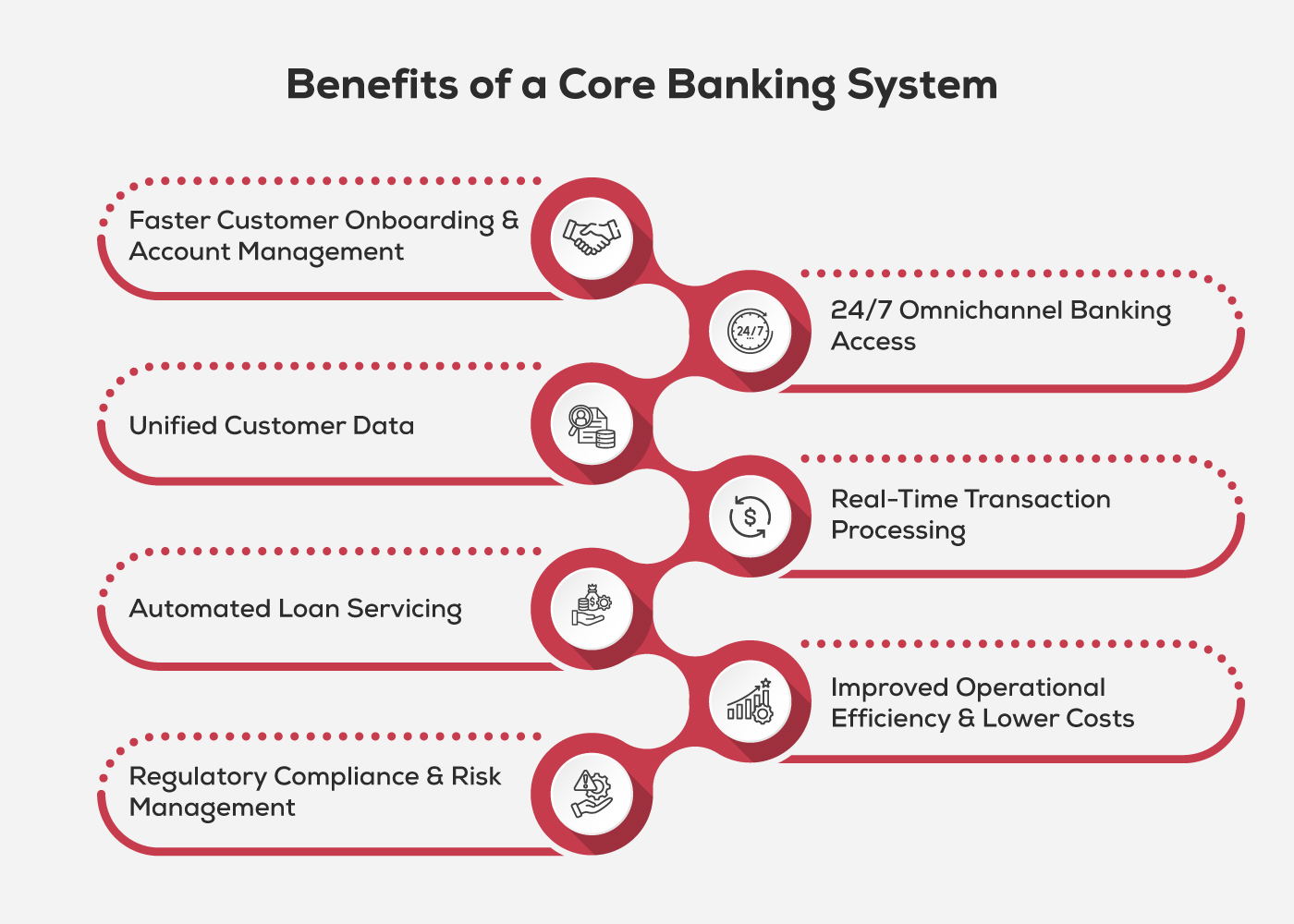

Benefits of a Core Banking System

Selecting the right core banking system is only part of the equation. A modern platform delivers measurable value across customer service, operational efficiency, compliance, and business growth. Some of the key benefits include:

- Faster Customer Onboarding & Account Management

A modern core banking system streamlines customer onboarding by digitizing account opening, identity verification, and account management processes. This reduces turnaround times, minimizes manual intervention, and enables financial institutions to deliver a smoother onboarding experience while maintaining accuracy and compliance.

- 24/7 Omnichannel Banking Access

Customers expect uninterrupted access to banking services across branches, internet banking, mobile applications, ATMs, and other digital channels. A core banking system enables consistent access to accounts, transactions, and banking services across these touchpoints, allowing customers to bank anytime while ensuring a seamless experience regardless of the channel used.

- Unified Customer Data

A centralized customer information repository provides a single, consistent view of customer profiles, accounts, and transaction history across the institution. This improves data accuracy, simplifies customer servicing, supports informed decision-making, and eliminates data silos across banking operations.

- Real-Time Transaction Processing

Real-time processing enables customers and bank personnel to access the latest account information immediately after transactions are completed. It also supports faster payment processing, improves transaction visibility, and enhances responsiveness across banking operations.

- Automated Loan Servicing

A core banking system automates loan servicing by managing interest calculations, repayment schedules, penalty assessments, and payment processing throughout the loan lifecycle. This reduces manual effort, improves accuracy, and ensures consistency in loan administration.

- Improved Operational Efficiency & Lower Costs

By automating routine banking processes and standardizing workflows, a core banking system improves operational efficiency across the institution. Reduced manual intervention, streamlined processes, and better integration with enterprise systems help lower operational costs, increase employee productivity, and enable teams to focus on higher-value activities.

- Regulatory Compliance & Risk Management

A modern core banking system supports compliance by maintaining accurate records, generating comprehensive audit trails, and facilitating regulatory reporting. It also strengthens operational governance by improving data integrity, traceability, and oversight, helping financial institutions manage regulatory and operational risks more effectively.

Top Core Banking Software Solutions

Several core banking platforms are available today, each offering capabilities tailored to different banking models, deployment strategies, and business requirements. The right choice depends on factors such as the institution's size, digital transformation goals, regulatory environment, and integration needs. Some of the leading core banking software solutions include:

- Infosys Finacle

- Temenos Transact

- Oracle FLEXCUBE

- TCS BaNCS

- Finastra Fusion Essence

- Thought Machine Vault Core

- Mambu

Why Choose Inspirisys

Delivering high-quality financial services today requires the support of a capable and experienced core banking solutions provider. A well-implemented Core Banking System enables banks and financial institutions to enhance service quality and stay competitive in a rapidly evolving landscape.

As a trusted Finacle delivery partner, Inspirisys brings deep domain expertise and a proven track record in implementing effective core banking solutions for a diverse set of clients. Our approach focuses on tailoring CBS deployments to meet specific business needs, supported by strong proficiency in Finacle tools, services, and core banking architecture. This enables seamless integration of banking operations and improved coordination across systems.

A thoughtfully designed Core Banking System can transform the way your organization operates by delivering better customer experiences, enabling modern banking capabilities, and streamlining processes through a centralized framework. Connect with us to elevate your digital banking services and unlock greater operational efficiency.

Frequently Asked Questions

1. How long does it typically take to implement a core banking system?

Implementation timelines can vary significantly depending on the size of the institution, complexity of existing systems, and scope of transformation. It may range from several months for smaller deployments to a few years for large-scale, multi-phase modernization programs.

2. Can a core banking system be implemented without disrupting existing operations?

Yes, many banks adopt phased or parallel implementation approaches to minimize disruption. Techniques such as gradual migration, sandbox testing, and hybrid coexistence with legacy systems help ensure continuity of services during the transition.

3. How important is data migration in core banking transformation?

Data migration is one of the most critical and complex aspects of CBS implementation. Ensuring data accuracy, consistency, and security during the migration process is essential to avoid operational risks and maintain customer trust.

3. What role does cybersecurity play in selecting a core banking system?

Cybersecurity is fundamental. A robust CBS should include advanced encryption, threat detection, and compliance with global security standards to safeguard sensitive financial and customer data against breaches and fraud.